Roberto Daffinà, Giovanni Finocchiaro

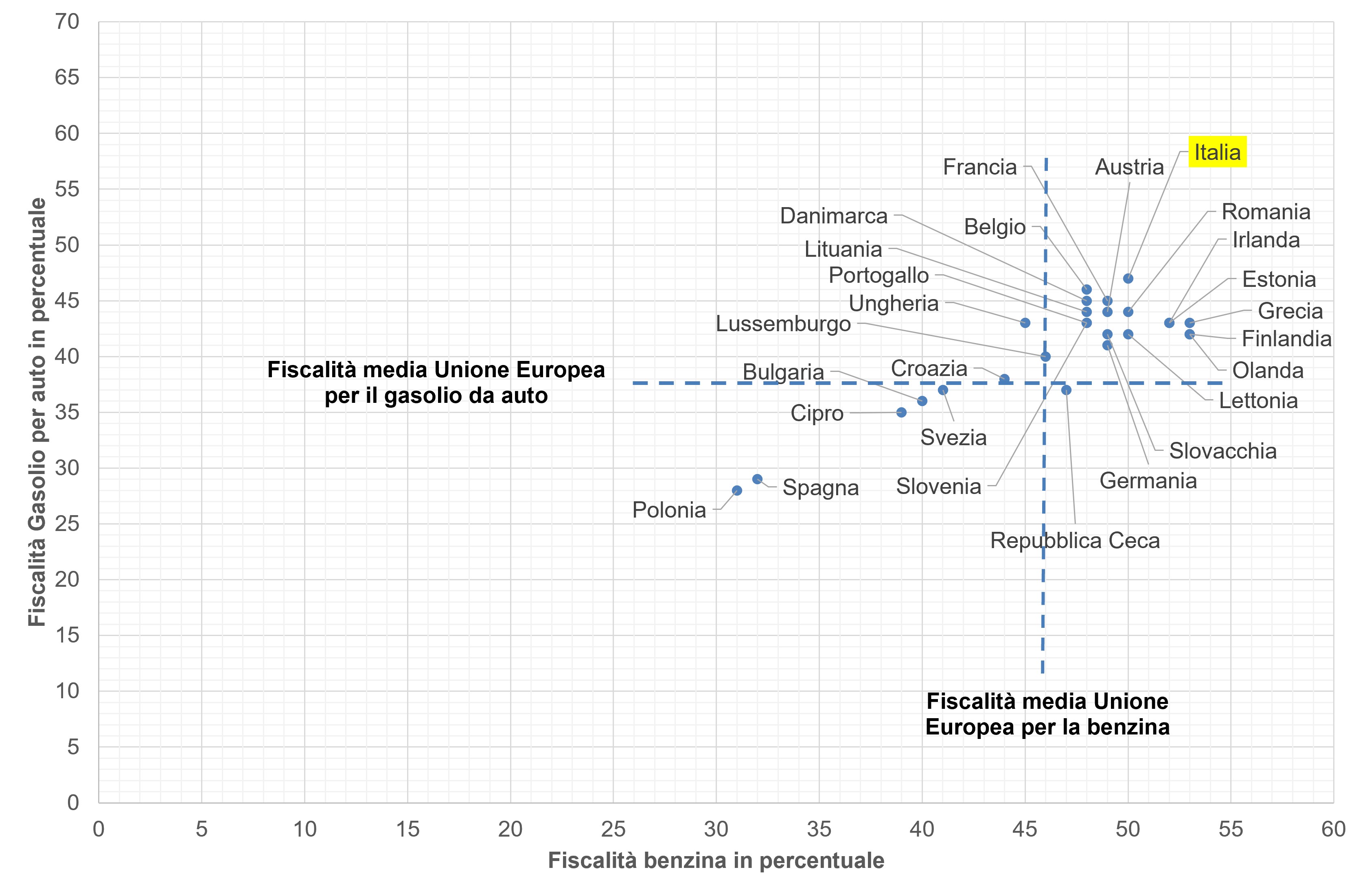

The indicator allows us to evaluate to what extent taxation levels correspond to external costs and favor the use of cleaner products, to move towards a pricing system that better incorporates environmental costs. With regard to the fiscal taxes applied in European states, in May 2026, Italy was in third place for petrol (50% incidence) and in first place for automotive diesel (47% incidence). Petrol is taxed at 53% by Greece, Finland and the Netherlands and 52% by Estonia and Ireland. The European Union average for petrol is 46% while for diesel it is 40%.

The information provided by the indicator is not directly related to the environmental situation, however the indicator is an indicator of the TERM (Transport and Environment Reporting Mechanism) system, created by the European Environment Agency and the European Commission at the request of the Cardiff European Council in 1998 and measures the tax collection in transport, which influences the effectiveness of transport policy. The main taxation element consists of fuel taxes, which are closely related to travel and carbon dioxide emissions, but poorly related to the main categories of external costs, i. e. Accidents and congestion.

Assess the extent to which taxation levels correspond to external costs and encourage the use of cleaner products, to move towards a pricing system that better incorporates environmental costs.

Infrastructure taxation is historically regulated by Legislative Decree 25 January 2010, n. 7 (and the subsequent Legislative Decree no. 43/2014 implementing Directive 2011/76/EU). However, the European framework has been profoundly renewed by Directive (EU) 2022/362 (the new Eurovignette Directive ), which exceeds the old criteria. This directive requires the transition from old time stamps to tolls calculated on distance and introduces a strong differentiation of tariffs based on CO2 emissions and the environmental performance of heavy vehicles, stringently applying the "polluter pays" principle to internalize the external costs of air and noise pollution.

The regulation of excise duties is contained in the Consolidated Law pursuant to Legislative Decree no. 26 October 1995. 504 (TUA). Over time, in addition to the transpositions of Directives 2003/96/EC and 2008/118/EC, the TUA has been the subject of a profound and structural rewriting by Legislative Decree 28 March 2025, n. 43 (Excise Reform). This reform has digitized and simplified the obligations, modified the tax moment for electricity based on actual consumption, redefined the categories of use of natural gas (now divided between "domestic" and "non-domestic") and introduced the qualification of SOAC ( Accredited Obliged Party ) for operators with high fiscal reliability.

With regard to excise duties on fuels, in addition to the continuous monitoring for the realignment of the rates (including the progressive alignment between diesel and petrol required by environmental constraints), the Regions remain entitled to decide on increases in the regional tax on petrol (IRBA) to deal with states of emergency. In fact, the energy taxation system continues to have a dual function: on the one hand, stabilizer of public accounts and extraordinary financing tool for emergencies (as in the past interventions of Law no. 122/2012 and Law no. 98/2013); on the other, fiscal leverage to guide consumers towards products with a lower environmental impact, in synergy with the new European systems for penalizing emissions (such as the extension of the ETS2 system to fuels for road transport).

For the taxation of biofuels, see the indicator "Diffusion of alternative fuels".

Objectives set by the legislation:

The current legislation - both Italian and European - provides very specific objectives that are guiding a structural reform of transport taxation. The underlying objective is no longer just to "raise cash" for the State, but to use taxes as an environmental lever for the ecological transition, applying the European principle of " the polluter pays ".

These objectives are set by three major regulatory and strategic pillars linked to the National Integrated Plan for Energy and Climate, the European "Eurovignette" Directives and the tax legislation on refunds.

The PNIEC (National Integrated Plan for Energy and Climate) is the programmatic document with which Italy implements the European targets for 2030. In terms of transport and taxation it provides for the realignment of fossil excise duties with the progressive elimination of the so-called Environmentally Harmful Subsidies (SAD). The goal is to eliminate the historical tax advantage of the most polluting fuels. The start of the realignment of excise duties between petrol and diesel (introduced with Legislative Decree no. 43/2025) responds exactly to this mandate. Achieving decarbonisation targets: Italy must reduce emissions in non-ETS sectors (including transport) by 43.7% by 2030 compared to 2005 levels. Taxation must discourage the use of traditional fuels in favor of electric carriers and advanced biofuels (such as certified HVO, which in fact enjoys a protected tax regime).

The reform of EU Directive 2022/362 establishes very clear objectives for road taxation, in particular for heavy vehicles: tolls linked to CO emissions 2 in which Member States must vary user fees (tolls and vignettes) based on the carbon dioxide emission class of the vehicle. Those who use zero-emission vehicles (electric or hydrogen) must obtain a toll discount of between 50% and 75%. Furthermore, the legislation requires the inclusion of a fixed quota in motorway tolls linked to the cost of air and noise pollution generated by the vehicle, effectively forcing the logistics sector to renew its fleets.

The tax legislation on refunds (like the commercial diesel that we analyzed before) has the explicit objective of accelerating the replacement of the fleet in circulation by excluding Euro 4 or lower vehicles from the tax benefits, the State uses fiscal leverage to force road haulage companies to scrap obsolete vehicles. The new European rules on state aid in the transport sector (which came into force in March 2026 with the TBER regulation) simplify tax bonuses and public support, but only if the funds are oriented towards multimodal solutions (rail + road) or very low-emission vehicles.

Ministry of the Environment and Energy Security, open data updated weekly

European Commission, open data updated weekly

Unione Petrolifera, Various years, Annual report

A weakness of the indicator is that it focuses on fuel taxation in road transport.

MASE (Ministry of the Environment and Energy Security), European Commission

Ministry of the Environment and Energy Safety, Energy statistics and weekly petrol price survey https://sisen. mase. gov. it/dgsaie/

European Commission https://energy. ec. europa. eu/data-and-analysis/weekly-oil-bulletin_en#documents

National

1996-2026

The data are provided by the Ministry of the Environment and Energy Security: The average prices are an average weighted with monthly consumption.

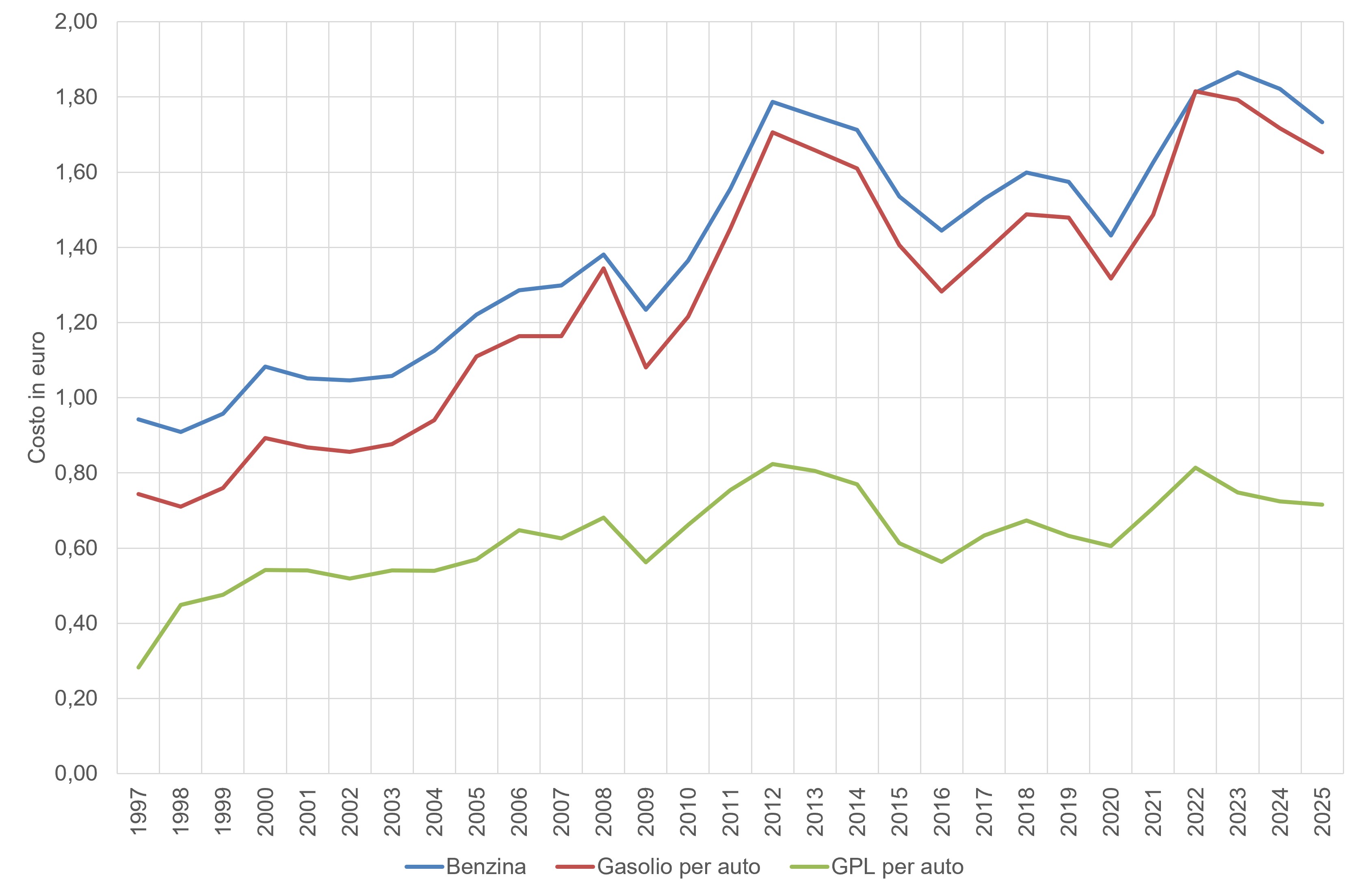

The price picture at the beginning of June 2026 highlights the strong impact of the figures on consumers' pockets starting from petrol which reaches an overall price of €1,951.51 per 1,000 litres, equal to approximately €1.95/l, where the fiscal component has a heavy impact with an excise duty of €622.90 and a VAT of €351.91 which leave a net industrial price of €976.70 €. This situation is overcome by car diesel whose total price reaches €2,019.43 per 1,000 litres, or approximately €2.02/l, a value determined by a very high industrial net equal to €1,082.37 to which are added a taxation with an excise duty of €572.90 and a VAT of €364.16. To close the scenario, the convenience of LPG is confirmed which remains the cheapest choice at €813.53 per 1,000 litres, approximately €0.81/l, a low cost thanks to a very low excise duty of €133.52 and a VAT of €146.70.

The analysis of the history from the end of 2023 to June 2026 highlights very distinct dynamics starting from petrol which shows a strong long-term upward trend despite recording a recent slowdown, in fact after falling to a minimum of around €1.62/l at the beginning of January 2026 it undertook a very rapid climb in the months of April and May, reaching €1.96/l even if the last week of the report at 01/06/2026 shows a slight reversal of course with a negative variation of -12.45 € per 1,000 litres. Moving on to diesel, we note a volatile and sharply increasing trend in the last month with diesel experiencing fluctuating dynamics but with a clear final surge given that between 18 May and 1 June 2026 it went from €1,982.73 to €2,019.43, recording a net jump of +€30.11 in the last week. Closing the picture is LPG which shows a stabilizing or decreasing trend, moving against the trend of traditional fuels since after having reached peaks of over €0.84/l in mid-May in the last period it has shown constantly negative variations, dropping to €0.81/l.

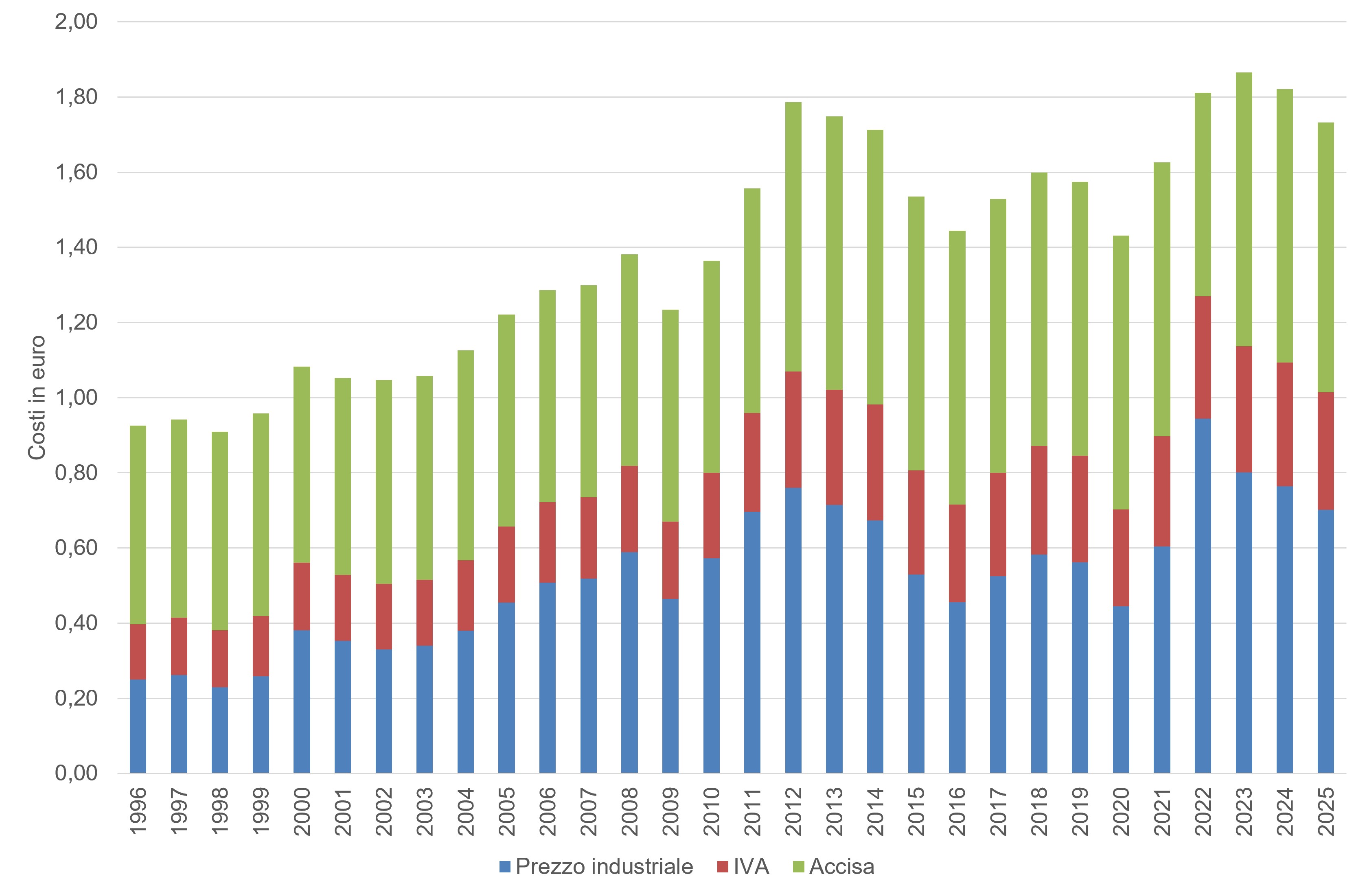

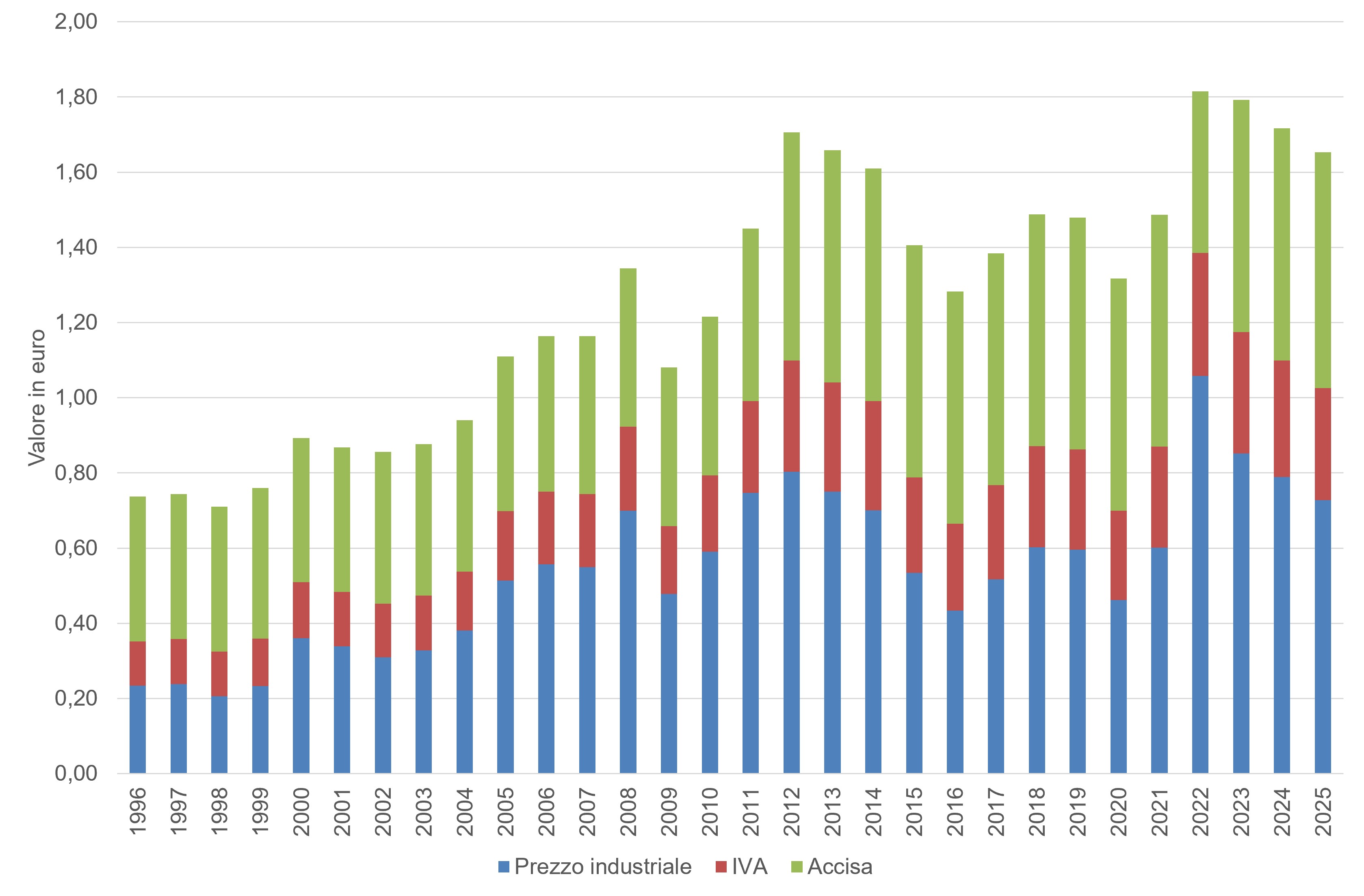

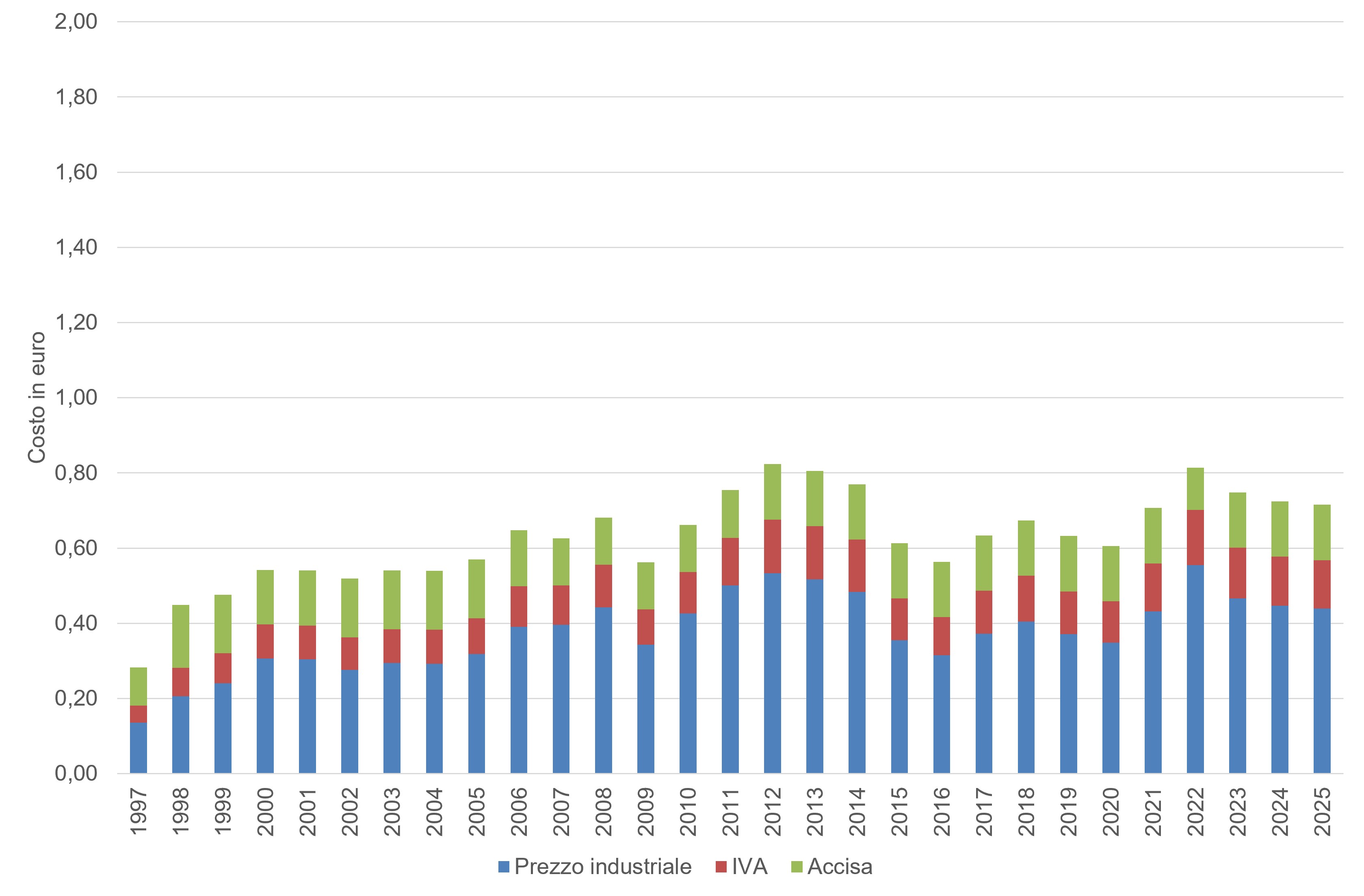

Industrial prices (consumer prices net of the tax component) expressed as average values for the year 2025 are equal to 0.70 euros/litre for petrol, 0.73 euros/litre for automotive diesel and 0.40 euros/litre for automotive LPG. Compared to the previous year, industrial prices recorded reductions of 8% for automotive petrol and diesel and 2% for automotive LPG. In the medium/long term, compared to 1997, industrial prices have recorded much more significant increases (+168% petrol; +206% automotive diesel; +224% automotive LPG). In 2025 in Italy the average annual consumer price of unleaded petrol, equal to 1.73 euros/litre, is made up of 0.72 excise duty plus 0.31 VAT plus 0.70 euros/litre industrial price (Figure 2); car diesel, consumer price equal to 1.65 euro/litre, is made up of 0.62 excise duty plus 0.30 VAT and 0.73 euro/litre industrial price (Figure 3); automotive LPG, on the other hand, is 0.15 excise duty, 0.13 VAT and 0.44 euro/litre industrial price for a consumer price of 0.72 euro/litre (Figure 4). Therefore, in 2025 the tax component on petrol is 1.03 euros/litre, that on diesel is 0.92 euros/litre while on automotive LPG it is approximately 0.28 euros/litre.

Please remember that the excise duty is a fixed tax that weighs on the quantity of goods produced net of regional additional taxes, while VAT affects the value of the products subject to excise duty and weighs on the excise duty itself. In this regard, in 2025, the overall tax component (sum of excise duties and VAT) on the price of petrol is approximately 60% (48% in 2022 and 75% in 1998), on the price of diesel it is approximately 56% (42% in 2022 and 71% in 1998) while on automotive LPG it is approximately 39% (32% in 2022 and 54% in 1998).

| Allegati |

|---|

Thumbnail

Headline

Figura 1: Prezzo al consumo, in euro, per 1 litro di benzina, gasolio per auto e GPL per auto Data source

Elaborazione ISPRA su dati del MASE |

Thumbnail

Headline

Figura 2: Composizione prezzo di 1 litro di benzina Data source

Elaborazione ISPRA su dati del MASE |

Thumbnail

Headline

Figura 3: Composizione del prezzo di 1 litro di gasolio per auto Data source

Elaborazione ISPRA su dati del MASE |

Thumbnail

Headline

Figura 4: Composizione del prezzo di 1 litro di GPL per auto Data source

Elaborazione ISPRA su dati del MASE |

Thumbnail

Headline

Figura 5: Incidenza della fiscalità sui prezzi della benzina e del gasolio per auto Data source

Elaborazione ISPRA su dati del MASE |

For 6 years from 1 January 1994 to 31 December 2020 the Regional Tax on Petrol for Motor Vehicles (IRBA) was in force. In which the first Regions (such as Piedmont, followed closely by many others in subsequent years) approved their own regional laws to make it operational. Initially it weighed 30 lire per liter (then increased to a maximum of 50 lire, equivalent to approximately 2.5 euro cents). The tax was definitively repealed by the State with the 2021 Budget Law (Law no. 178/2020), which imposed a stop starting from the first day of the year to close the dispute with the European Union. Even though the state law covered that period, not all regions implemented it in the same years. Since it is an optional tax, some Regions introduced it immediately in 1994, others activated it much later (such as Puglia in 2012), while some Regions have never applied it or had suspended it before 2021 so as not to penalize local distributors near regional borders.

With regard to automotive diesel used in the transport sector, the following are entitled to benefit from reimbursements of the increases in the excise duty rate provided for by current legislation:

Access to the benefit is subject to a strong environmental limitation: diesel consumption by Euro 4 or lower category vehicles is strictly excluded from the reimbursement. In order to submit the application, the vehicles must belong to the Euro 5 environmental class or higher and the vehicle license plate must be indicated on the electronic fuel purchase invoice.

With reference to more recent consumption, following the reform of the rates and emergency decrees on energy prices, the extent of the benefit recognizable per thousand liters of product is remodulated and fragmented on a quarterly basis by the Customs and Monopolies Agency. In the first quarter of 2026, for example, the amount of the reimbursement is equal to €269.68 per thousand liters for standard diesel fuel (calculated on the basis of the ordinary rate of €672.90), a figure which drops to €69.68 in the periods in which temporary emergency cuts to the excise duty at the pump are triggered, while for the certified eco-sustainable HVO biofuel the benefit is permanently set at € 214.18 per thousand litres.

From 1 January to 18 March 2026: Legislative Decree no. Came into force. 43/2025 on the realignment of rates, which raised the ordinary excise duty on diesel fuel to €672.90 per thousand litres. To keep the cost of commercial diesel borne by transporters unchanged, the reimbursement was raised to the record figure of €269.68 per thousand litres.

From 19 March to 31 March 2026: The government intervened urgently with the Legislative Decree. N. 33/2026 (so-called "Fuel Decree") to cut prices at the pump, lowering the general excise duty to €472.90 per thousand litres. As a result, the Customs Agency reduced the reimbursement rate for these 12 days to €69.68 per thousand litres, as the deduction needed to reach the protected rate for road haulage was lower.

From the comparative data on excise duties applied in the European Union states, net of the temporary tax reduction measures introduced by individual governments, Italy firmly confirms itself at the top in Europe for the tax burden on fuels, positioning itself among the top three member countries for percentage incidence of taxes (excise duty + VAT) on the final consumer price for both petrol and diesel. In figure 5, Italy, in May 2026, is in the third band for petrol (incidence equal to 50%) and in first place for automotive diesel (incidence equal to 47%). Petrol is taxed at 53% by Greece, Finland and the Netherlands and 52% by Estonia and Ireland. The average for European Union countries is 46% for petrol while for diesel it is 40%.